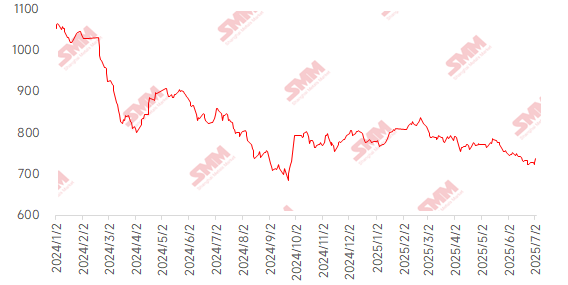

This week, imported iron ore prices surged significantly, with the price center moving upwards, primarily driven by positive news and improved market sentiment. The June PMI's MoM increase indicated a sustained improvement in manufacturing sector prosperity. The significant YoY growth in special-purpose bond issuance in H1 reflected enhanced government support. Additionally, the "anti-cut-throat competition" policy sparked market expectations for potential supply-side reforms at the important July meeting, jointly boosting market confidence. On the industrial fundamentals front, steel's apparent demand increased slightly, and total inventory buildup was limited. The unremarkable supply-demand imbalance provided support for prices. Iron ore futures prices rose significantly, but the relatively weaker spot market led to an expansion in the spread between futures and spot prices. In terms of port spot prices, the weekly average price of PB fines at Shandong ports increased by 10-15 yuan/mt WoW.

Chart: SMM 62% Imported Ore MMi Index

Source: SMM

This week, domestic ore prices rose slightly. It is expected that domestic ore prices will still have a slight upward space next week. In Tangshan, Qian'an, and Qianxi of Hebei, prices increased by 5-10 yuan/mt. In west Liaoning, Chaoyang, Beipiao, and Jianping, prices increased by 1-5 yuan/mt. Prices in east China were basically stable.

In the Tangshan area of Hebei, the price of local mine iron ore concentrates was relatively stable. The dry-basis, tax-inclusive delivery-to-factory price for 66% grade ore was 870-880 yuan/mt. Traders and steel mills showed improved enthusiasm for purchasing at individual lower prices. Local mine transactions increased, and prices showed an upward trend. However, the local mines and beneficiation plants were facing relatively tight resources, providing some support for local iron ore concentrate prices. Steel mills currently had moderate profits, providing some support for the demand for iron ore concentrates.

In west Liaoning, iron ore concentrate prices rose slightly. The wet-basis, tax-excluded ex-factory price for 66% grade ore was 680-685 yuan/mt. Various inspections were relatively frequent in the area, and the overall production resources of iron ore concentrates were relatively tight, providing some support for local ore prices. On the demand side, steel mills were mainly purchasing as needed, and the overall desire to bargain down prices remained strong. In the short term, the tug-of-war between sellers and buyers in the market was relatively evident.

In east China, mines and beneficiation plants were mainly operating normally, with current inventory pressure not being significant. They were mainly selling as they produced. From a pricing perspective, the average price index of imported ore this week increased slightly WoW, and it is expected that prices may rise slightly.

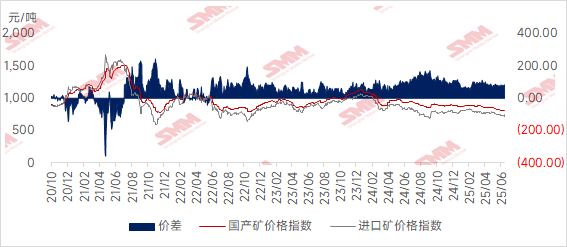

Chart: Price Spread Between Imported and Domestic Ores

Source: SMM

Looking ahead to next week

For imported ore: Looking ahead to next week, iron ore prices are expected to continue holding up well. Despite a marginal weakening in fundamentals, overseas shipments may continue to rebound due to the push for target at quarter-end, and port arrivals still have room to increase. The supply side will maintain a growth trend. Demand side, although environmental protection-driven production restrictions in Tangshan have suppressed sintering machine production, the impact on blast furnaces has been limited. Coupled with moderate steel mill profits, pig iron production will remain high. Although port inventories have accumulated slightly, the extent of inventory buildup has been limited, exerting a weaker suppressive effect on prices. The current market sentiment is optimistic, and coupled with fundamental support, there is still enthusiasm for long positions. However, caution should be exercised regarding potential market disruptions as the deadline for tariff negotiations approaches, as well as the risk of further tightening of environmental protection-driven production restriction policies in the north.

Domestic ore perspective: Overall, the price increase of domestic iron ore concentrates compared to imported ore prices has not been significant this week. The price spread between domestic and imported ores has narrowed, and the cost-effectiveness of domestic ores has improved compared to the previous period. Coupled with the overall tight supply of resources, there is certain support for ore prices. Steel mills' overall production enthusiasm remains strong, and it is expected that domestic iron ore concentrate prices may have some upward potential next week.

》Click to view the SMM Metal Industry Chain Database

![[SMM Steel] European carbon prices hold above €70/t amid ETS reforms and CBAM signals](https://imgqn.smm.cn/usercenter/NtHAJ20251217171719.jpg)

![[SMM Steel] India’s FY2025-26 crude steel output rises, exports surge while imports fall](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)

![[SMM Steel] SAIL to launch hydrogen injection at Bokaro blast furnace to cut emissions](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)